The Risk Parity Line: Moving from the Efficient Frontier to the Final Frontier of Investments

Article 4 of 7

Executive Summary

- Each of our sub-funds (Alpha, Beta and Gamma) provides risk parity because the weight of each asset in the corresponding portfolio is set to be inversely proportional to the risk derived from investing in that asset. This can be equivalently stated as equal risk contributions from each asset towards the overall portfolio risk.

- Investors can select their desired level of risk or return and allocate their wealth accordingly among our sub funds, which balance one another under different market conditions. This evolution of the risk parity principle, resulting in a mechanism that is geared to do well under all market cycles, brings more robust performance and can be termed as conceptual parity.

- The inclusion of newer and more diversified assets into our portfolios, as the crypto landscape expands, can be viewed as a natural progression from the conventional efficient frontier to a progressive final frontier of investing, which will continue to transcend itself.

Risk Parity is the holy grail that we originally set out to bring to the decentralized investment world. To obtain parity, the amount of money allocated to the individual assets in a portfolio has to be proportional to the extent of risk encountered from investing in that specific asset. As the risk characteristics of an asset fluctuate, the weight assigned to that asset has to be correspondingly modified.

A subtle aspect of our portfolio construction and VVV weight calculation methodology [LINK] is that parity is already accomplished in each of our individual funds Alpha, Beta and Gamma. Our investment products, (Alpha, Beta, Gamma and Parity) will provide risk managed access to several crypto assets and strategies. We have adapted many of the well known safety mechanisms and investor protection schemes that have evolved for several decades in traditional finance, and combined them with many innovations that are unique to crypto markets.

Having mentioned that each of our sub funds already achieves risk parity, we need to draw a distinction between mathematical parity and conceptual parity. The assets weights are calculated based on precise rules and mathematical operations and this brings parity to each of our sub funds at the asset level. While this is still a huge innovation to bring to the blockchain environment, we wish to proceed further and bring parity also on a conceptual level.

To elaborate further, we create portfolios that perform satisfactorily where mathematics can fall short of completely combating market uncertainty. Broad categories of assets have slightly different risk and return attributes. By grouping assets with similar responses to different market regimes, we can ensure that the various groups counterbalance one another under diverse market conditions. Hence, in addition to mathematical parity, within each sub fund, each sub fund has an overall risk return feature which is preferable to the other sub funds under a particular market criterion.

Another motivation for creating these groups is because even if assets at the individual level deviate from their risk and expected return properties, such a misalignment is less likely at the group level. A few assets in a bunch might display atypical behavior, but the majority of them will be closer to their representative qualities. The result is that the overall group can be expected to behave in a certain way and offset other groups, which are constructed based on the same principle of clubbing together similar assets, that have different attributes. We term this fluctuating pseudo-equilibrium between groups of assets conceptual parity.

A remarkable idea from the financial markets is that of the efficient frontier. There are many ways to combine assets to create portfolios. Among all the possible combinations the set of combinations that are superior to the rest, in terms of risk and expected returns, form the efficient frontier.

Despite the efficient frontier being an intriguing idea, there are many practical limitations to accomplish this. To ensure that we are not constrained by the many reservations, our innovation has been to come up with the idea of conceptual parity tailored for the crypto environment. With this modification, Alpha will be a sub-fund composed of assets that provide higher returns and take on higher risks. Beta will be representative of the larger market behavior and provide more steady returns with a correspondingly lower level of risks. Gamma will take on the role of acting as the risk free rate, with decent returns but with very little to no risk. Gamma will also be filled with assets that demonstrate negative correlation to Alpha and Beta assets.

The implication of constructing the sub-funds (Alpha, Beta and Gamma) in this way ensures that when the overall market under performs, which means Alpha and Beta will not deliver very high returns, Gamma will still continue to provide acceptable returns because of its negative correlation to Alpha and Beta. The manufacturing, and linking, of Alpha, Beta and Gamma will then produce the most efficient set of portfolios in terms of risk and return characteristics. We term this collection of portfolios, the parity line.

We believe that the efficient frontier is a moving target, even in the traditional financial world, with assets being added or removed, their risk-return properties undergoing alterations and even entire markets getting transformed. This is all the more the case with the rapidly evolving crypto landscape, where many new protocols and projects are appearing on the scene.

We will be adding several blockchain protocols to our investment funds, becoming a highly diversified cross chain collector of wealth appreciation venues. Our plans to add more protocols will be discussed in the last and seventh article of this series. In addition, we will continuously evaluate new projects and, if they pass our due diligence standards, include them in our portfolio. We will also add exposure to derivative instruments and physical assets such as gold, real estate, and so on, as and when they become available. The implication of this is that our investors will be getting better returns and lower risks, as we seek out varied sources of risk adjusted returns.

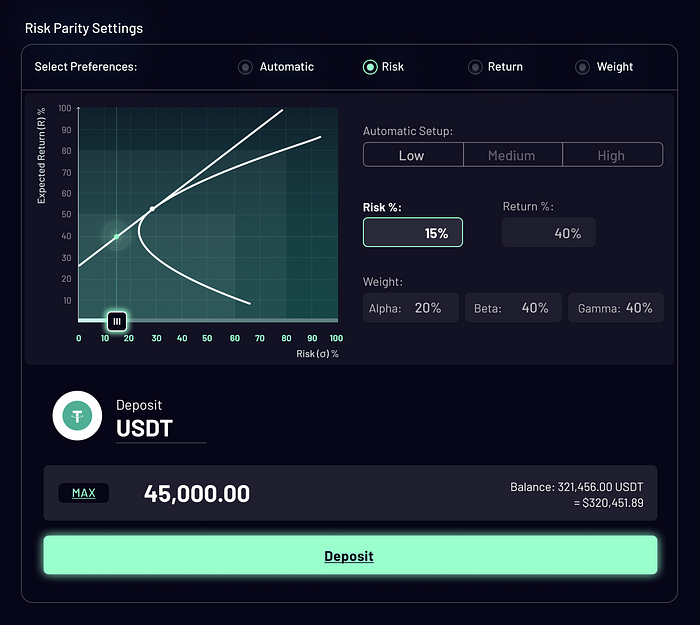

The user experience has been designed such that investors can tailor their wealth allocations to their preferred risk appetites. Users can select either their preferred level of risk or return. Investors can also directly decide how much of their wealth they want to allocate to the three funds: Alpha, Beta and Gamma. Once either of the three routes are selected, (Risk or Return or Weights of Alpha, Beta and Gamma), the other parameters are automatically calculated and saved into an NFT, which the investor will hold for the life of the investment.

The preferences can be changed anytime by investors and this will trigger a readjustment of their sub fund allocations. Our investment specialists will also monitor the markets and, as the relationship between risk and return changes, will fine tune the parameters of the parity line and update the parameters of the portfolio allocations. This will guarantee that all investors are getting the best possible outcomes customized for their desired wealth management objectives.

The challenge was to ensure that the user interactions are intuitive, and yet their preferences are precisely captured in the investment decisions. This has been accomplished by letting someone who does not wish to be bothered with all the settings, or a novice investor, have the simple option of choosing the default, depositing his funds and forgetting about everything else. If this is the option chosen, the portfolio will select a low level of risk and calculate the other parameters accordingly. Advanced users can choose their risk level or their expected return, or the weights they want to assign to each of the sub funds. The other parameters will be automatically calculated.

The outcome of these innovations is an investment machinery that responds to investor preferences and adapts to changing market conditions. In addition, our vehicles will adhere to the core tenets of decentralization and be accessible by anyone. The next, and fifth, article will discuss our plans to share a significant portion of the profits we generate with our community. All of this can be viewed as a natural progression from the conventional efficient frontier to a progressive final frontier, which will continue to transcend itself.

Figure A: Deposit Screen for Parity is an illustration of our pioneering efforts to bring investors the tools to grow their wealth tailored to their risk appetites. Please note that the following figure is an early draft version. Since our team is still putting some finishing touches to the user interface, there might be some changes to this design before it is made available to everyone for actual usage.

Our Socials

Website: https://formation.fi

Telegram: https://t.me/FormationFi

Twitter: https://twitter.com/FormationFi

Medium: https://formation-fi.medium.com